Reverse Mortgage Questions

How Do I Qualify For A Reverse Mortgage?

To become eligible for a reverse mortgage, you must be at least 62 years old and own your home. You must have equity in the house to pay off any outstanding balances, and your home must be occupied as your principal residence. All applicants are subject to a financial assessment to determine their financial capacity and willingness to pay obligations as part of the qualification process.

How Much Money Could I Get?

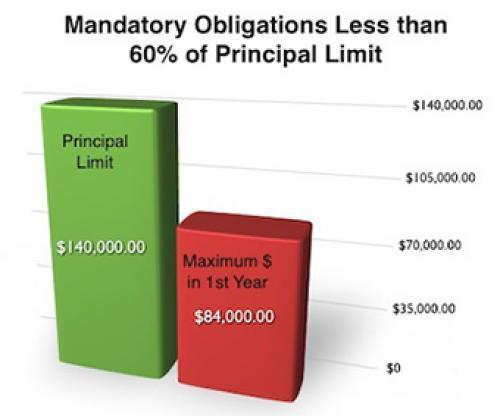

The amount of money that a lender will loan depends on how old you are at the time of closing, how much your house is worth, the total amount of liens, and interest rates. The payoff of your existing mortgage and mandatory obligations along with the payment option chosen will affect the amount of money you will receive. HUD limits borrowers to using 60% of the available money (after closing costs & fees) in the first year. The remaining funds are accessible beginning year two. This maximum disbursement limit set by HUD allows for the GREATER of:

- 60% of the Principal Limit (amount of money available to the borrower in all years of the loan) in the first twelve months of the loan from your closing date OR…

- The sum of Mandatory Obligations (existing mortgage payoff, tax liens, closing costs, mortgage insurance premium) plus 10% of the Principal Limit. This total cannot exceed the total Principal Limit at the time of loan closing.

How Do I Receive My Money?

There are several different options to choose from. You can take the money in a lump sum (up to HUD’s first-year maximum withdrawal)*, set up a line of credit, monthly payment, or a combination of all three. In the first year, the Line of Credit or monthly Tenure Payments or monthly payments cannot exceed 60% of the Principal Limit. After the first year, the available Line of Credit or Tenure/Monthly payments will be increased when applicable.

* Fixed interest rate reverse mortgages only allow for the Single Disbursement Lump Sum payment plan.

What Costs Are Associated With A Reverse Mortgage?

The fees and cost of a reverse mortgage are based on a number of items. For example, an origination fee is paid to the broker/lender, a MIP (mortgage insurance premium) is paid to FHA on the Home Equity Conversion Mortgage (HECM), an appraisal fee, a flood certification fee, a document preparation fee, title, settlement, and escrow fees. All costs are clearly shown on the Good Faith Estimate (GFE). Monthly servicing fees could apply.

What Are The FHA Mortgage Insurance Premium Charges?

FHA requires a Mortgage Insurance Premium (MIP) to be collected at closing and during the life of the loan. These premiums are charged to the borrower's loan balance. The upfront Mortgage Insurance Premium (MIP) is calculated using your home's appraised value or a maximum of $1,249,125 (the 2026 national HECM limit cap) and is charged at closing. The ongoing FHA insurance premiums are calculated using each month's outstanding loan balance.

Is It Required That I Receive Counseling Before Getting A Reverse Mortgage?

Yes. Counseling is required with an independent third party HUD-approved counselor to protect borrowers from receiving incorrect information about reverse mortgages. The lender must be in receipt of the counseling certificate before they can close the loan. To locate a reverse mortgage counselor near you, contact your Mortgage Loan Originator or your local HUD office.

Do I Get Taxed On The Money I Receive From My Reverse Mortgage?

While the proceeds you receive from a reverse mortgage are typically not subject to individual income taxation, you will need to consult your tax advisor.

Do I Have To Pay Any Fees To The Reverse Mortgage Lender During The Course Of My Loan?

A reverse mortgage was created so borrowers don’t have to pay most fees during the course of the loan. Typical upfront costs are for the appraisal and HUD-approved reverse mortgage counseling (some agencies waive counseling fees at their discretion). However, there may be a monthly servicing fee associated with reverse mortgages (which will be financed and added to the loan balance). For more information on the service set-aside, please talk to your Mortgage Loan Originator.

*These FAQs are not from HUD or FHA and have not been approved by HUD, FHA or any federal government.

Resources

AARP free information on reverse mortgages

Phone: 1-800-209-8085

The Consumer Financial Protection Bureau (CFPB) Consumer Lookup

http://www.nmlsconsumeraccess.org/

Housing Counseling Clearinghouse

Phone: 1-800-569-4287

The Eldercare Locator: Local Resources for Older Adults

http://www.eldercare.gov

Phone: 1-800-677-1116

Federal Trade Commission (FTC) to report possible fraud

http://www.ftc.gov

Phone: 1-877-FTC-HELP (1-877-382-4357)

National Council For Aging Care

http://www.aging.com/

Phone: 1-877-664-6140